![]()

on December 11, 2021, 1:21 pm

on December 11, 2021, 1:21 pm

BLUE LINE = BRLUSD

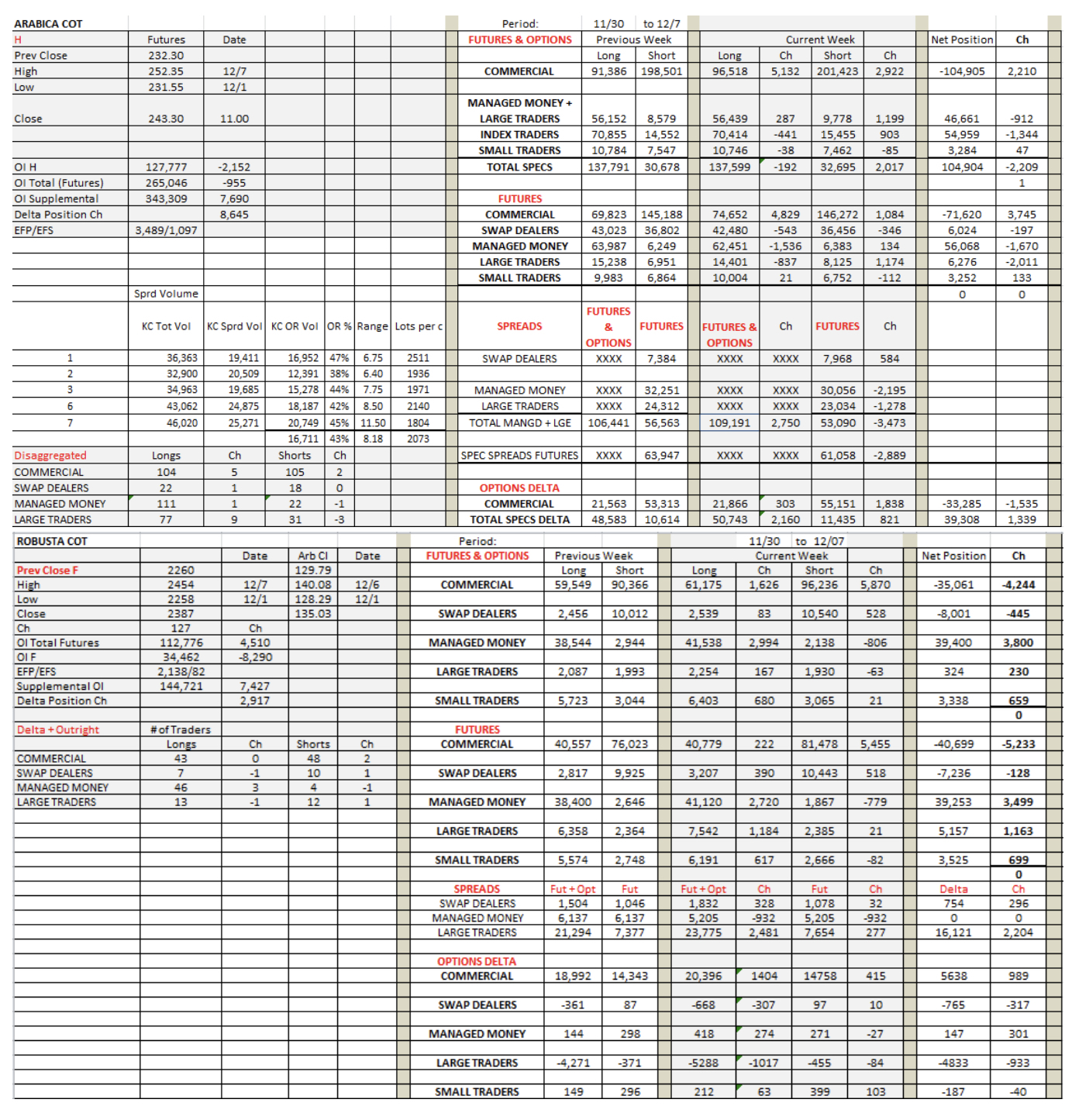

The market began at the lows of the COT period, made a high of 252.35, set a range of 20.80c for the period, dropped sharply on the last day of the report and closed 11.00c higher. The days following the report, prices continued to drop to end the week at the same level as the beginning of the period. Analyzing the report continues to be difficult as a result of the bidirectional moves.

Commercials were net buyers. Did they buy on the way up? Or, did they sell as prices rose then reversed as prices dropped on the last day? Funds were on the opposite side of the commercials. Knowing that KC managed money are mostly motivated by momentum, it is likely that they were initially buyers and reversed on the last day. Note that index again sold. Large traders sold the most. Does their activity represent the undoing of delta short covering? Its great to write options, but in a volatile market delta maintenance becomes difficult. Oddly, the RC report is the opposite of KC for the most part. There the spec groups increased their positions while commercials sold.

Spreads continue to be exciting as CSO implied volatility and actual volatility climbed. In RC, the FH began in the 60s and moved sharply higher. The highest that I saw it was 120 but it may have been higher. It seems to have been partially motivated by F short covering against forwards as the F OI dropped and the total OI rose. On Friday, FH ended at 85. In KC, the K2K3 began at 2.15, K2 premium of course, moved to a high of 7.80, keeping its value as prices eased except for Friday when it closed at 5.85. HK however had plenty of resistance. It moved higher to a high of 1.10 and closed on Friday at .25. Of course, weakness in the HK was foreseeable as the H OI is naturally the highest of the delivery months. It has been slowly dropping.

The market is now in an area where it may remain for a bit before it takes off again higher. I remain cautiously bullish.

Message Thread

![]()

« Back to index