![]()

on April 9, 2022, 12:40 pm

on April 9, 2022, 12:40 pm

BLUE LINE = BRLUSD

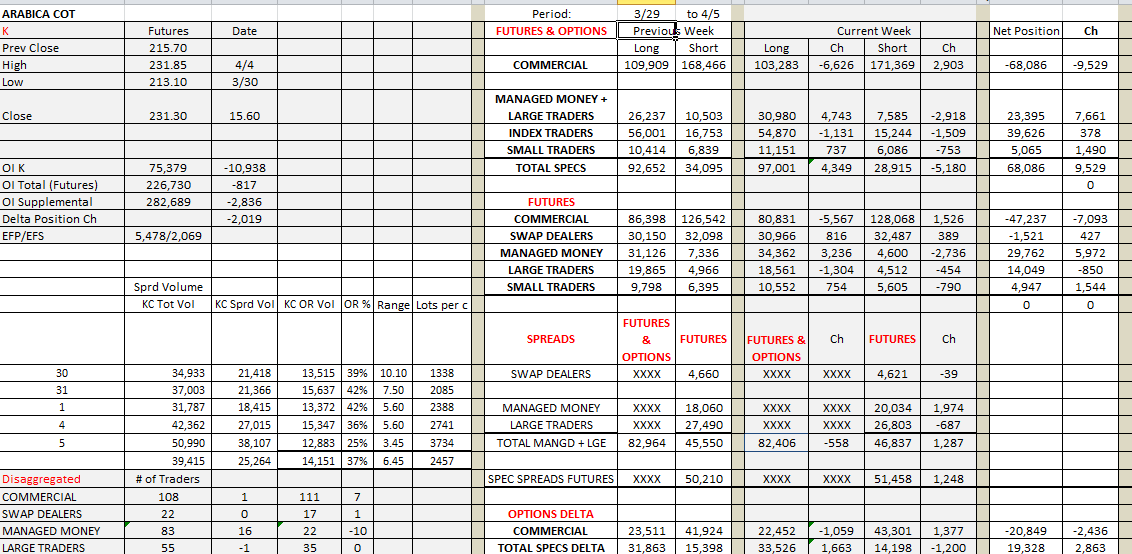

Prices were steady throughout the entire COT period as funds were emphatic buyers. Ten funds covered shorts and 16 funds bought, resulting in an 18.75c move from low to high and a net change of 15.60c. Small traders bought as well while commercials were the primary sellers. The roll shows that as K was liquidated, the total OI hardly changed indicating that traders are content with their positions. Option expiration was responsible for any interruption in direction near striking prices.

The days following the COT report, began with weakness but obvious resistance. On the last day of the week, the market began near the lows and proceeded higher, likely propelled by continued fund buying and covering by delta shorts. Whatever the reason, the market ended on a firm note. Whether we have seen the usual option expiration dip is uncertain however.

Spreads behaved in a dull manner. The KN was .10 bid, not very impressive. The bulk of the OI is likely liquidated in K. NU remained weak and will likely continue weak now that KN CSOs have expired. Expiration shows the many disenchanted traders. In KN 16,770 calls were abandoned and 16,525 puts, many of the puts were part of a fence position where puts were sold and calls were bought. The highest strike purchased was 5.00c. The KU CSOs look relatively similar with the highest call purchased at 7.00c.

There were no surprises in outright options.

Message Thread

![]()

« Back to index