![]()

on June 18, 2022, 12:05 pm

on June 18, 2022, 12:05 pm

BLUE LINE = BRLUSD

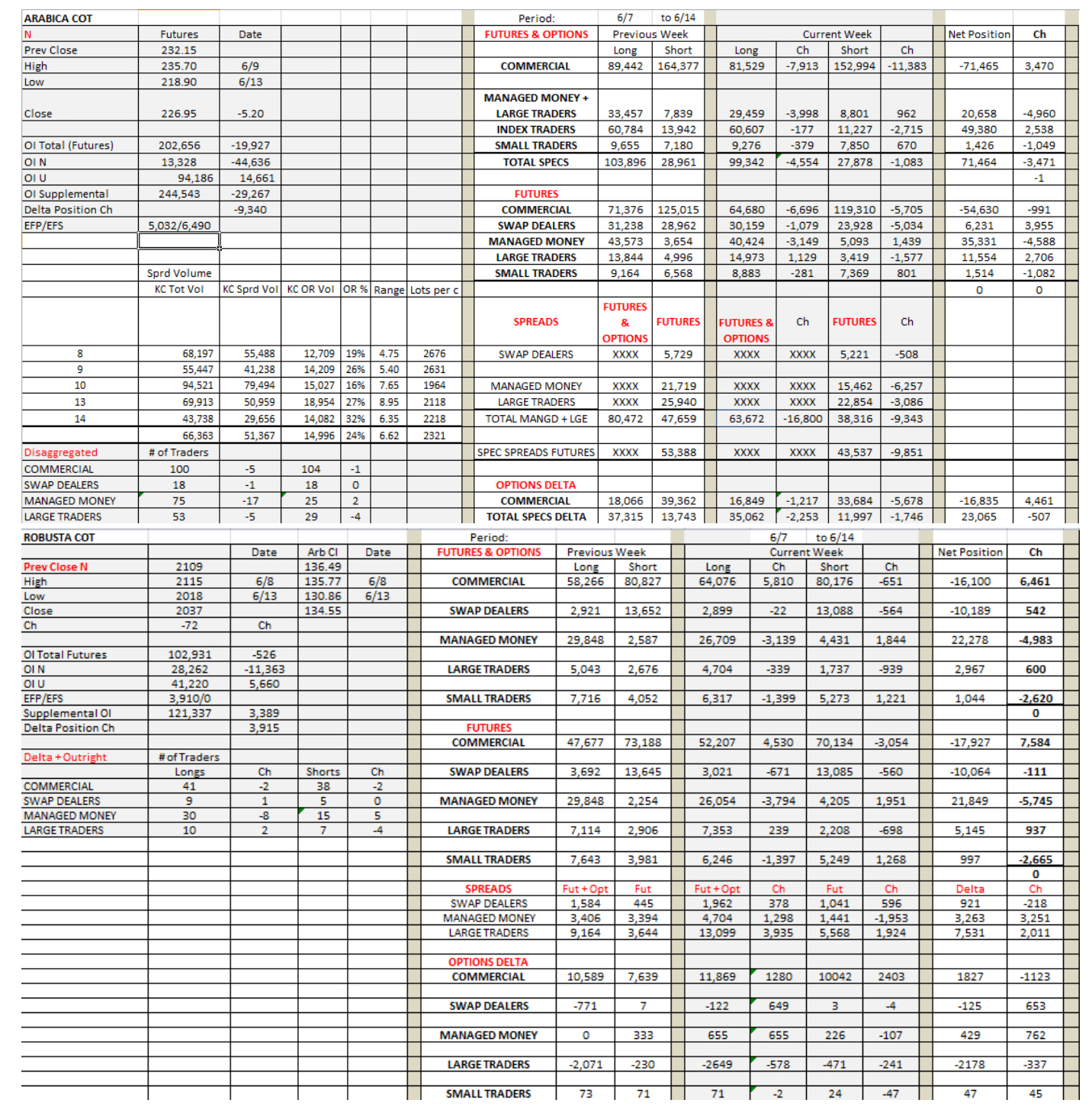

Prices began on a weak note, rallied, and sharply dropped during the days surrounding option expiration. After a drop of 16.80c from the highs, the market firmed and registered a 5.20c negative change for the COT week. Although U is now the lead month, the period began with a relatively active N. Outright volume was light as it remained in the teens but the N option expiration and N roll were heavy. As the N OI dropped sharply, U did not gain as much. Yet the U OI is higher than N was while K was being rolled. The changes in the COT reflect mostly the results of option expiration. Once again we see the impact on the market as specs scramble to hedge calls and market makers try to even their delta positions. Its difficult to analyze the COT report because of expiration but we see that managed money liquidated 17 long funds and added two short funds as a result. RC renders a clearer picture that we can apply to KC as well as option expiration there isnt until the 21st. Managed Money liquidated heavily, joined by Small Traders as commercials bought.

The remainder of the week looked promising for bulls. Friday may have reflected day trade liquidation at the end of day. Still, longs and commercials kept a lid on the market and provoked the weakness that we saw. It remains a spec driven market while it appears, at least for now, that fundamentals are already in the market. But it would help the long side if ICE lowered margins and if equities were not suffering as they are.

Spreads are merely following outright prices but UZ may start to show some weakness at some point. For now winter is starting on the 21st and specs seem to be preparing for the possibility of crop damage. The U volatility is presently the highest implied volatility on the board at 37.85%. The UZ has been steady and the U OI is climbing and may break 100k. Also a steady indicator is Index who again added to to their long position.

Message Thread

![]()

« Back to index