![]()

on July 9, 2022, 5:27 pm

on July 9, 2022, 5:27 pm

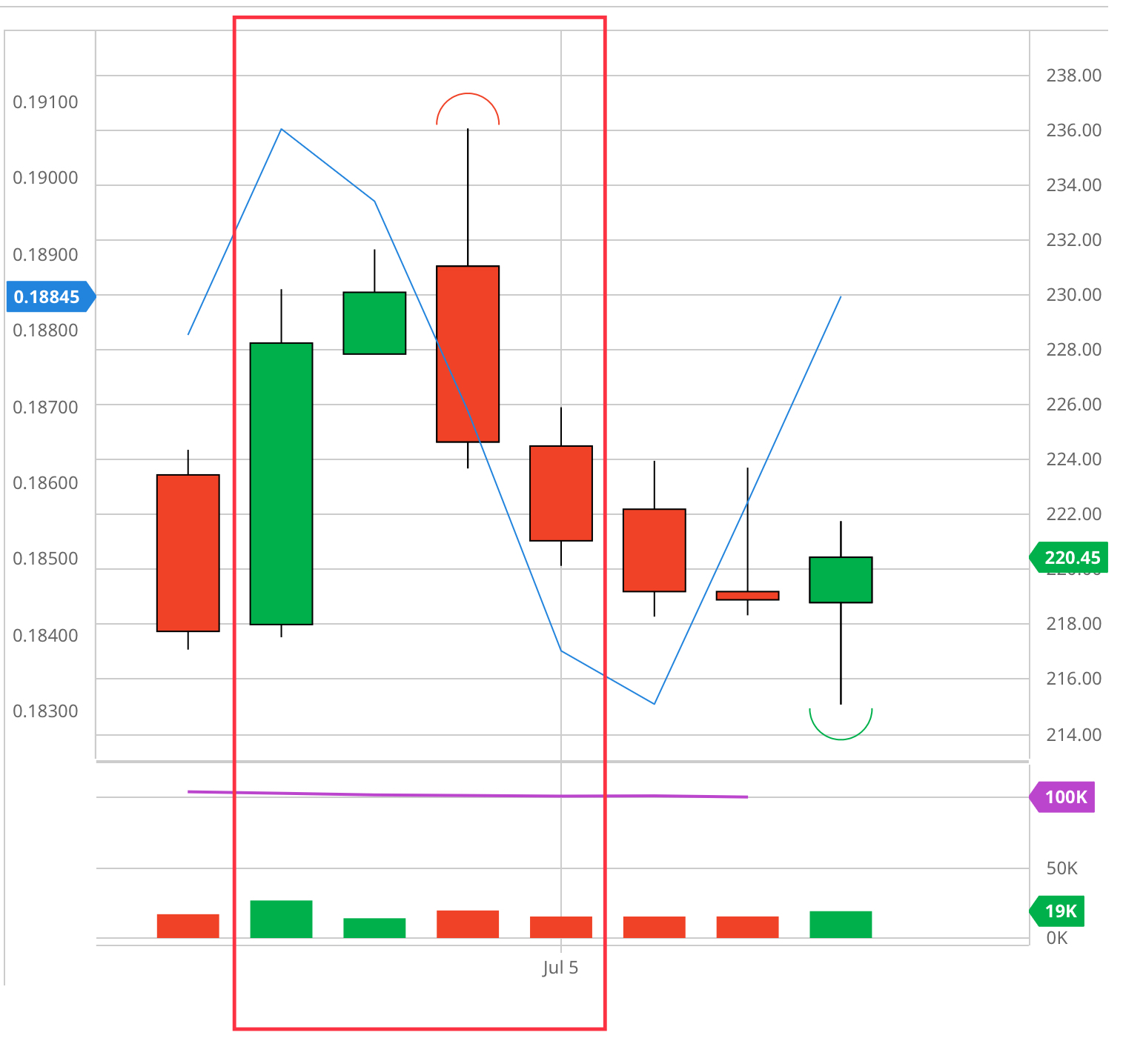

BLUE LINE = BRLUSD

The market began strongly on the first day of the COT report, followed by a second day of strength. By Friday of last week, prices hit 236.05 which proved to be the high of the period as it opened the gates to sellers. The market collapsed that same day and continued to weaken the following week. Surprisingly, prices closed higher from the previous COT period by 3.30c with a range of 18.50c for the period. On Friday, yesterday, the market made a low of 215.10 and recovered slightly by the end of day, not quite reversing the momentum funds. Outright volume was small but by the end of the period it was higher than spread volume as spreads continue to be on the thin side.

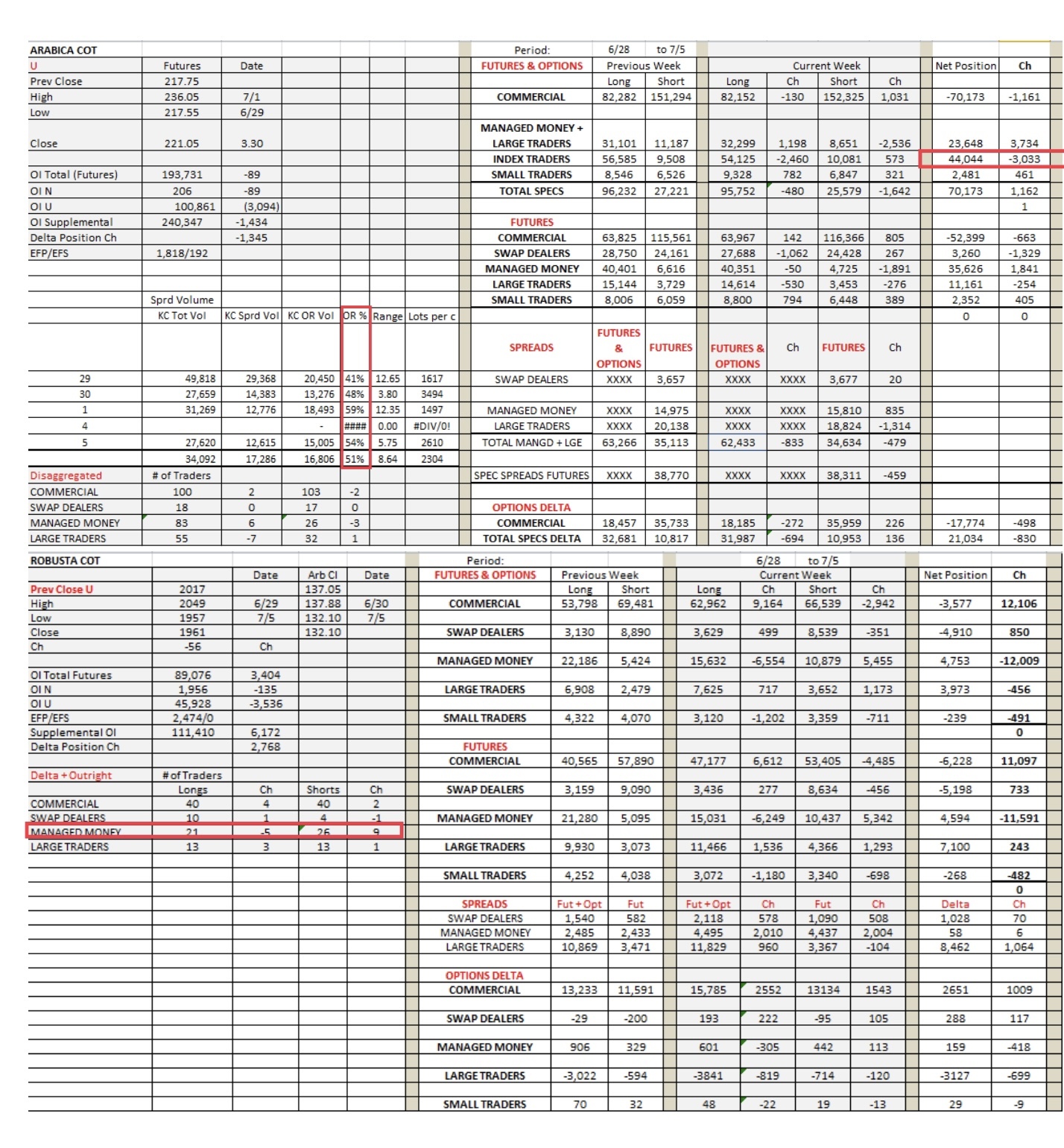

Because of the two way market that KC experienced, the changes of the sectors activity are small. What stands out however is the continued selling of some of the Index funds, whether as delta or futures which is a bearish sign. RC is a stark contrast to KC. There, the market began at the highs to end at the lows. Managed money, which are not momentum funds in RC, sold heavily, changing their stance from long to short, unlike KC funds which remain net long.

The market can certainly move higher but with the combination of sellers that we see, rallies appear to be selling opportunities. Spreads, on the other hand, show strength even as they ease, at least in the front three. Momentum funds should be sellers on Monday, depending where prices will be at 8:00. Regardless, their reversal trigger is not too far from yesterdays closing prices. Q options are off the board. The settlement price in U was 220.45 with a post close last trade of 220.00. 142 puts of the 220.00 strike were exercised while 508 puts were abandoned.

Message Thread

![]()

« Back to index