![]()

on July 23, 2022, 11:24 am

on July 23, 2022, 11:24 am

BLUE LINE = BRLUSD

The key word in the recent market is volatility. Volatility increased in the outright market, in spreads and in volatility itself.

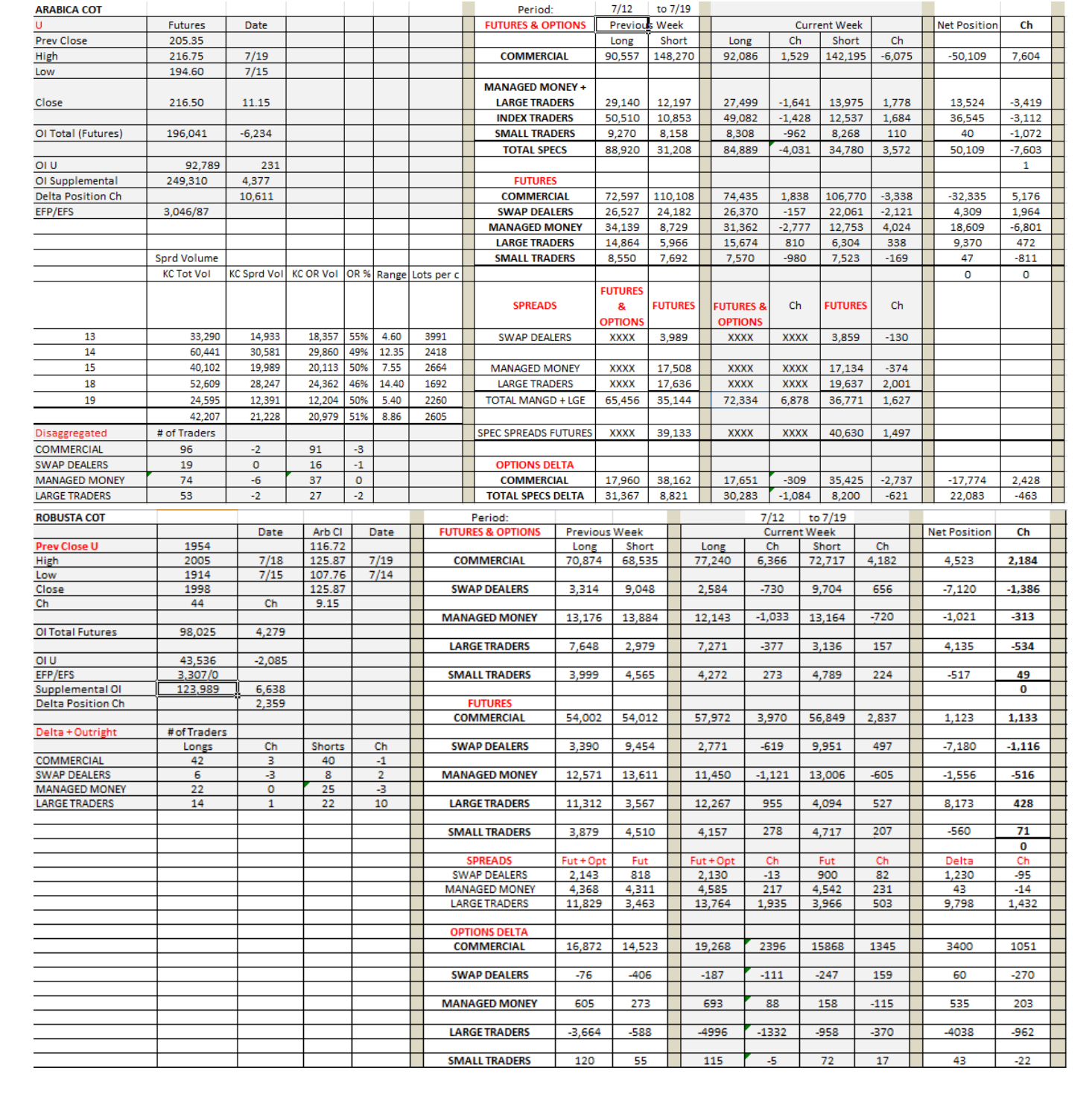

Prices began in a downtrend, breaking 200.00 and hitting a low of 194.60. It appears that below 200.00 consumer buying was present as large bids were hit in the forwards. Forward bids could be anyone but according to the COT swap dealers increased their buying which could be end users. After all, the forward markets provide great value for consumers, relative to the front months. The market then proceeded to rally 22.15c ,from low to high, to close 11.15c higher from the previous COT close. The report probably shows considerably smaller changes compared to what they were at the lows. But the numbers are still revealing. Index again sold heavily while commercials bought. Managed money sold as well. Origin did not appear to be selling in spite of the weak Real, unless the selling took place in the nearby months.

The supplemental shows that options were bought. As the futures OI dropped by 6,234 lots, the markets delta position increased by 10,611 lots, mostly with spreads in options. On the Friday of the COT, volatility closed at 42.85%, +5.9% from the day before, dropped sharply as specs and trade liquidated longs in both U futures options and CSOs. This Friday, U volatility closed at 36.95%, up 3.75% from the previous day. In spite of the selling in options, futures spreads not only held, but rallied. The UZ traded up to +4.35. Yesterday, the range in UZ was 3.75 to 4.35. It rallied as futures dropped, continuing the disconnect between futures and spreads.

The outlook of the market looks bleak as Index and other specs continue to sell in both markets. Attempts to rally, although worthy, are short-lived. The market could not even reach 220.00. Yet shortages in the near future seem to be real. Certified stocks are down to 705,727 bags. Spreads continue to be strong in the front. There were a mere 129 lots tendered but 91 lots were from Brazil which are settled at a discount to spot. Monday will bring a fresh market with funds in a selling mode. I remain negative for now.

The market has traditionally reacted to changes in warehouse stocks but only in spreads. If global stocks are in jeopardy or abundance, then the futures react as well. The forums production consensus tells us that we are at 58.7 mm bags for 2223, but this number includes several traditionally very low estimates, some extremely low. My guess is that production will be closer to 61mm bags, in line with Safras which is pretty reliable. What are global carryover stocks?

Message Thread

![]()

« Back to index