![]()

on August 6, 2022, 10:19 am

on August 6, 2022, 10:19 am

BLUE LINE = BRLUSD

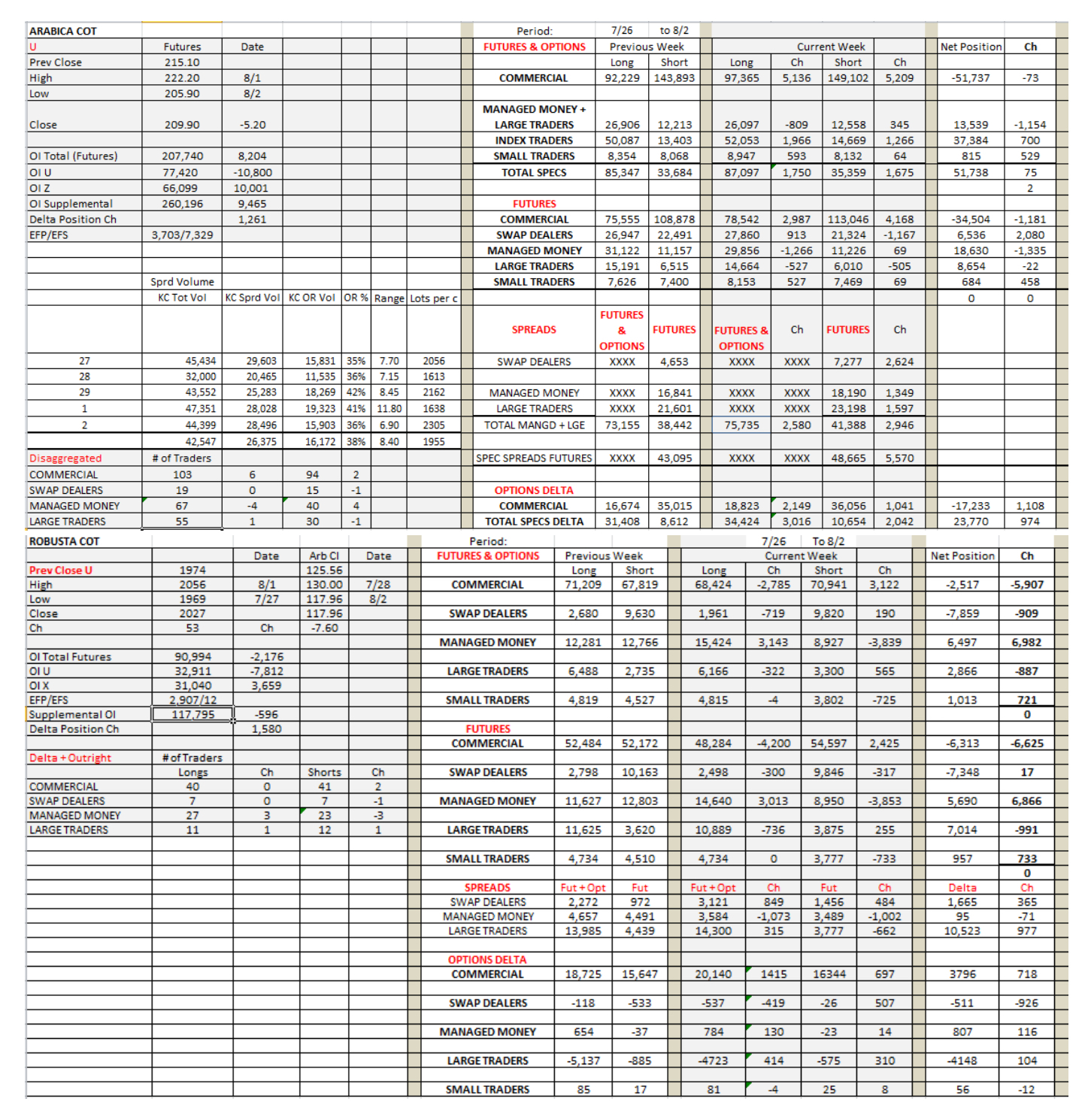

We again have a two-way market, with high volatility at times and light outright volume, which fell to as low as 35% of total volume. The net result is that we have only slight changes in the COT report once again, except for the RC report which shows substantial buying by managed money and almost equal selling by trade. The market was able to penetrate the 220.00 area, reaching a high of 222.20, but struggled to make new highs as resistance increased. The total range was 16.30c with a net change of -5.20c. Although the sector changes are minimal, there are some highlights in KC that are worth pointing out. The OI shows the continued rolling, which began in mid-July, of U into Z. The total OI increased indicating the greater activity of spreads. The days following the COT report, showed the same characteristics of the report week and remained within its range.

On Friday the 5th, Index funds began to roll their U positions. The anticipated strength by several players, as a result of the 29k drop of certified stocks, did not occur, quite the opposite. There was buying on the way down but buyer succumbed and turned sellers, as long liquidation continued and as momentum funds turned sellers. Spreads dropped in value with outright prices as the roll intensified but it seems that, the tail is wagging the dog. The UZ which has been weak for a while traded from around 3.80c to 3.00c, closing at 3.05c. The Z22/Z23 that had closed the day before at 14.45c, settled on Friday at 12.30c.

The dynamics of the market have not changed for a while. Specs send prices down to the lows and buy at the highs, with commercials happily on the other side. Consumer and origin presence is not evident or of little significance currently. At lower prices there may be consumer support but we may not see origin selling until spreads return to a discount, backwardation, market. If so, then producers have the luxury of once again selling forwards at a premium combined with high yields in the Selic.

Spreads continue to reflect certified stocks withdrawals but may not reflect global stocks, imo. Carryover stocks adequately cover any deficit that the production shortfall has created, compared to consumption, and as shown by the ICO reports. Coffee flow has decreased as a result of logistical and shipping issues. If so, domestic stocks of producing countries must be building, and so, certified stocks are falling, and so, spreads are generally steady but the outright market is not so steady.

This week may be more difficult to trade however. There will be continued U liquidation but option expiration shows that Puts outnumber Calls at current levels, causing unhedged puts to provide support. This, together with likely trade support at lower prices, should prevent any sharp fall, depending on the intensity of selling by futures longs. The U OI on Thursday the 4th was 71,563.

I dont usually make such bold remarks. So please do post any comments contradictory or otherwise. The fact remains that the market has no follow through either way.

Message Thread

![]()

« Back to index