![]()

on March 9, 2023, 7:56 am

on March 9, 2023, 7:56 am

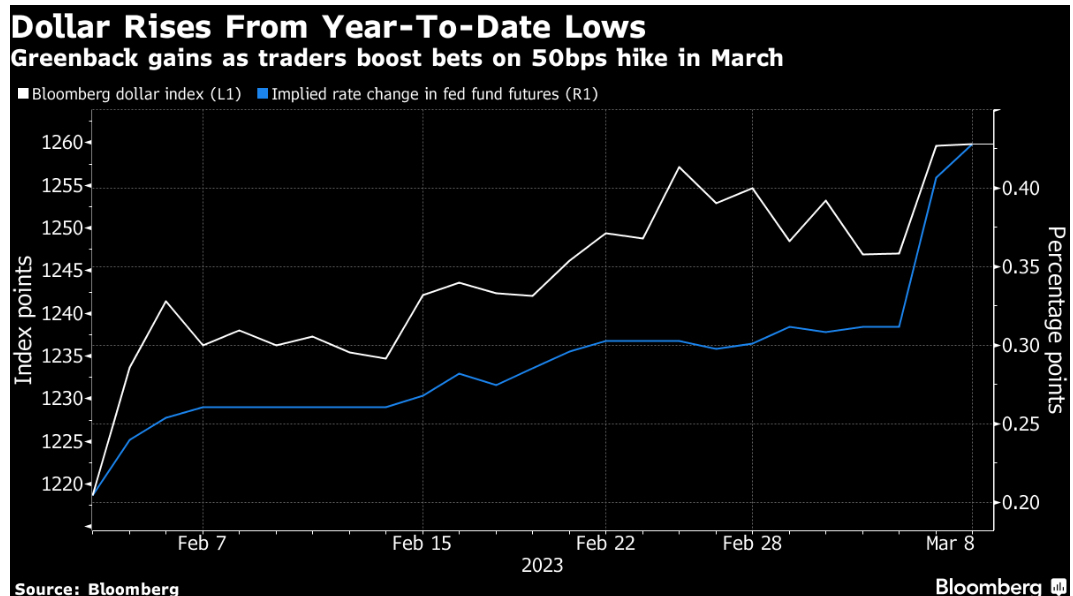

The dollar strength is a function of US rates expectations. Yes, sure, fine. We all know that and that's how it SHOULD work. Higher rates attract investment inflows, which supports the currency. Econ 101. Except that the Fed isn't working in isolation here. Where it goes, the ECB and others (BOJ excepted) will follow. So the carry argument makes a little less sense.

Perhaps what's really happening is a tail-wagging-the-dog effect. The dollar has been the de facto haven since the pandemic sell-off. Interest rate hikes raise the risk of a policy overshoot leading to a recession, which increases demand for the dollar, which puts pressure on dollar-denominated assets, creating (stretching the analogy) a dog-chasing-tail effect with an infinite loop of downward pressure on risky assets.

Or maybe it's just the nerves getting to me before jobs day.

Eddie van der Walt is Deputy Managing Editor in the Markets Live team, based in London. Follow him on Twitter at @EdVanDerWalt.

Message Thread

![]()

« Back to index